Your auto loan isn't just a way to pay for your car; it's the dealership's most profitable product and your most powerful negotiation lever. Most buyers walk into a showroom focused on the sticker price, but the real cost is often hidden in the fine print of the finance office. You might worry about being pressured into high APRs or junk fees that inflate your monthly payment. We understand that the dealership financing vs credit union choice feels overwhelming, especially when the average new car payment has climbed to $757 in 2026.

It's frustrating to feel like you're losing control the moment you step into the finance and insurance room. We believe you deserve a transparent, stress-free experience that prioritizes your financial health over a dealer's bottom line. This guide provides the clarity you need to secure the lowest interest rates, like the 3.89% APR currently offered by top credit unions, and shows you how to spot markups before they cost you thousands. You'll learn the specific strategies needed to bypass predatory lending tactics and finalize your purchase with the quiet confidence of a seasoned advocate.

Key Takeaways

- Learn why the finance office is a dealership's primary profit center so you're prepared for high-pressure sales tactics.

- Compare dealership financing vs credit union benefits to decide if the ease of dealer-arranged loans is worth a higher interest rate.

- Uncover the "Buy Rate" secret lenders offer dealers so you'll know exactly how much your loan is being marked up.

- Use a firm pre-approval from a credit union as your strongest leverage to keep your total loan costs as low as possible.

- Discover how expert advocacy removes the burden of negotiation, allowing you to focus on the excitement of your new vehicle.

Understanding the Financing Landscape: Dealership vs. Credit Union

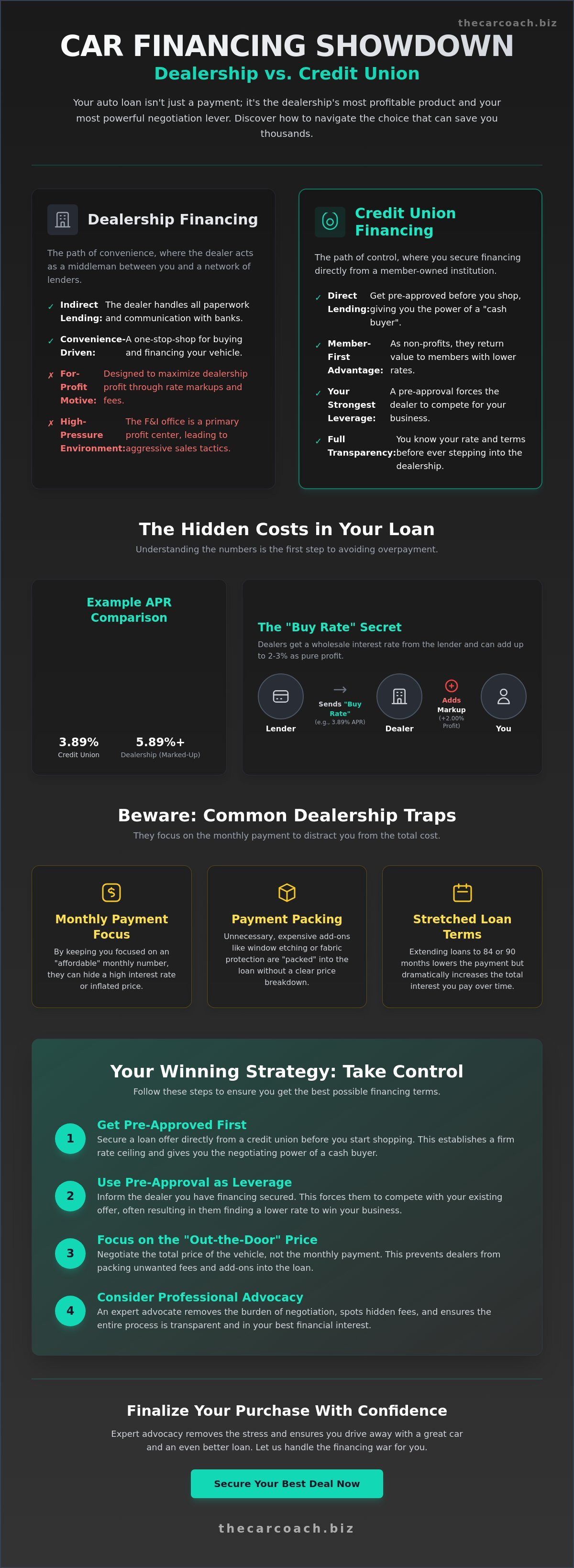

The showroom floor is where you choose your vehicle's color and trim, but the Finance and Insurance (F&I) office is where the dealership's real profit is made. For most retailers, the "back-end" of the deal generates significantly more revenue than the actual sale price of the car. This reality is why the choice between dealership financing vs credit union is the most important financial decision you'll make during the buying process. While a dealership is a for-profit entity motivated by commission and lender kickbacks, a credit union is a member-owned institution designed to return value to its participants. Understanding this fundamental difference helps you approach the desk with a sense of calm authority rather than anxiety.

Dealers often focus the conversation on your monthly payment to distract you from the total cost of the loan. By stretching out terms to 84 or 90 months, they can make a high-interest loan look affordable on a month-to-month basis. However, our goal is to help you look past the monthly figure to the total cost of credit. Securing the right financing isn't just about the rate; it's about maintaining control over the entire transaction so you aren't steered into a loan that benefits the house more than your household.

The Direct vs. Indirect Lending Model

Choosing a loan involves picking between two distinct delivery systems. Direct lending occurs when you secure a loan directly from a financial institution like your local credit union before you shop. This gives you the power of a "cash buyer" and establishes a firm budget. Conversely, indirect lending happens when the dealer acts as a middleman. They collect your credit information and send it to a network of lenders to find a match. For a deeper look at these structures, Understanding Car Finance provides a helpful overview of how these models evolved. Indirect lending is a convenience-based model that often carries a hidden cost.

Why Your Choice Impacts Your Total Car Price

Your financing choice dictates how much leverage you have to negotiate the vehicle's actual price. Dealers frequently use a tactic called "payment packing." By keeping you focused on a monthly number, they can easily slide in expensive add-ons like window etching or interior protection packages without you noticing the price hike. If you walk in with a pre-approved rate from a credit union, you strip away their ability to manipulate these numbers.

- Transparency: Pre-approval sets a ceiling on your interest rate.

- Negotiation Power: It forces the dealer to compete with your existing offer.

- Clarity: You see the true price of the car without the fog of financing math.

We provide financing negotiation as part of our purchase assistance because we know how easily these details can be blurred. When you have an advocate handling the financing negotiation, the dealer can't use your credit score as a tool to inflate their own profit margins. This professional buffer ensures your signing process is smooth, transparent, and entirely focused on your best interests.

Dealership Financing: The Convenience vs. The "Back-End" Profit

Walking into a dealership and driving out with a new car and a loan in a single afternoon is undeniably convenient. This efficiency exists because dealerships operate as a hub for dozens of different lenders, from national banks to local institutions. They handle the paperwork and the data entry, acting as a broker between you and the money. However, this convenience is rarely free. While you focus on the excitement of the vehicle, the finance manager is often focused on the "back-end" profit. This is the revenue generated after the price of the car is settled, and it's where the dealership financing vs credit union choice becomes a financial turning point for your household.

The atmosphere of the Finance and Insurance (F&I) office is carefully curated to feel professional and official, yet it's often the highest-pressure environment in the building. You've already spent hours picking the car and haggling over the price. By the time you reach the F&I desk, decision fatigue has likely set in. Dealers know this. They use this moment to present financing options that may look competitive on the surface but are designed to maximize the dealer's commission. Staying calm and informed is your best defense against being steered into a higher-cost loan than you actually qualify for.

The Mechanics of Rate Markups

When a dealer submits your credit application, the lender returns a "Buy Rate." This is the actual interest rate the lender requires based on your creditworthiness. For example, if the lender offers a Buy Rate of 7.04%, which was the average for a 60-month new car loan in May 2026, the dealer might quote you 8.5%. The difference is known as the "Dealer Reserve." It's a legal commission the dealer earns for arranging the loan. To protect yourself, always ask to see the Buy Rate. You can also consult the CFPB Auto Loan Guidance to better understand your rights regarding rate transparency and disclosures.

When Dealership Financing Wins

There are specific scenarios where the dealer can actually beat your credit union's offer. This usually happens through "captive lenders" like Toyota Financial or Ford Credit. These manufacturers offer subvented rates, such as 0% or 1.9% APR, to move specific inventory. If you have excellent credit, these incentivized rates are almost always the best financial choice. However, you must often choose between the low APR and a cash rebate. If the rebate is large enough, it might be cheaper to take the cash and use a higher-rate loan from your credit union. Our professional financing negotiation service can help you run these numbers to ensure you're making the most protective choice for your budget.

- Captive Lenders: Manufacturers use their own banks to offer rates that commercial banks can't match.

- Complex Credit: Dealers have relationships with subprime lenders that may be more flexible than traditional institutions.

- One-Stop Shopping: The ability to trade in a car and finance a new one in one place saves significant time.

Currently, the average auto loan rate sits around 9.45% across all lenders, so even a small markup can add thousands to your total cost over a five-year term. By understanding the dealer's motivation, you shift the power back to your side of the desk. You're no longer just a buyer; you're an informed consumer who knows the value of every percentage point.

Credit Unions: The Member-First Advantage in Auto Loans

When you shift your focus from a for-profit dealership to a member-owned credit union, the entire atmosphere of the transaction changes. Credit unions are not-for-profit cooperatives. This means their primary goal isn't to extract maximum profit from your loan, but to return value to their members through lower interest rates and reduced fees. When comparing dealership financing vs credit union options, the primary distinction lies in the organization's core mission. While a dealer's finance office is designed to be a profit center, a credit union functions as a financial ally. This structural difference is championed through Credit Union Advocacy, which ensures these institutions remain focused on the financial well-being of their members rather than corporate shareholders.

In May 2026, the average interest rate for a 60-month new car loan sits at approximately 7.04%. However, top-tier credit unions like Navy Federal have been able to offer rates as low as 3.89% for members with excellent credit. This gap isn't just a few dollars a month; it represents thousands of dollars saved over the life of your loan. Credit unions also evaluate "Loan-to-Value" (LTV) ratios with much more transparency. While a dealer might try to "roll in" negative equity or expensive add-ons that push your loan to 120% of the car's value, a credit union will often provide a reality check. They help you stay within a safe lending limit, protecting you from becoming "upside down" on your vehicle the moment you drive away.

The Power of Pre-Approval

Walking onto a lot with a "check in hand" or a digital pre-approval completely changes the power dynamic. It simplifies the negotiation to a "cash price" discussion, preventing the dealer from using monthly payment math to hide the car's actual cost. In the 2026 digital landscape, this process is faster than ever. Most credit unions now offer instant pre-approvals through their mobile apps. You can apply while sitting in the showroom and have loan funding ready on your phone before the salesperson returns with their first offer. This allows you to set your budget based on real, verified numbers rather than dealer estimates.

Personalized Service and Lenient Criteria

Credit unions often look beyond just a FICO score. They consider your history as a member and your overall financial health. This personalized approach is especially beneficial if you're buying an older pre-owned vehicle. While many commercial banks reject loans for cars over seven years old, credit unions often provide competitive terms for high-quality used cars. You'll also find that secondary products like Gap insurance or extended service contracts are significantly cheaper at a credit union. Dealers often mark these products up by 200% or more, whereas your credit union typically offers them at a transparent, low-margin price. We often help clients through Pre-Owned Vehicle Purchase Assistance to ensure they're matching the right car with these superior member-only benefits.

The Hybrid Strategy: How to Use Both for the Lowest APR

You don't have to choose a single side in the dealership financing vs credit union debate. In fact, the most financially savvy buyers use both. By treating your credit union pre-approval as a baseline rather than a final destination, you force the dealership to compete for your business. This hybrid approach turns the finance office from a place of pressure into a competitive marketplace where you hold the winning hand. We've seen this strategy save our clients significant money by stripping away the dealer's ability to dictate terms based on your lack of options.

The process begins with securing a firm pre-approval from your credit union, but the secret lies in when you reveal it. Keep your financing "cards" close to your chest while you negotiate the actual price of the vehicle. If a dealer knows you have outside money, they might be less willing to budge on the car's price because they know they won't make a profit on the loan. Once you've settled on a fair purchase price, only then should you invite the dealer to attempt to beat your credit union's rate. This methodical progression ensures you get the best price on the car and the best terms on the money.

Negotiating the Rate, Not Just the Price

When the finance manager presents their initial offer, use a specific, calm phrase: "I have a pre-approval at X.X%, can you beat that?" This simple question shifts the burden of labor onto the dealer. Every dealership has a "floor rate," which is the absolute lowest APR the lender allows them to offer without adding a markup. If they want your finance business, they'll often drop to this floor rate to keep the deal in-house. Don't worry about the "credit pull trap" during this stage. As long as all credit inquiries for an auto loan occur within a short window, typically 14 to 45 days, credit scoring models treat them as a single event to allow for healthy rate shopping.

Analyzing the "Fine Print" in 2026

Before you sign, you must compare the "Truth in Lending" disclosures from both sources side-by-side. Look past the monthly payment and examine the total finance charge and the length of the term. A 1% difference in APR can save thousands over a 60-month term. Be wary of dealers who offer a lower payment by stretching the loan to 84 or 90 months, as this significantly increases your total interest cost and keeps you in a position of negative equity longer. Verify that there are no prepayment penalties, which allows you the freedom to refinance or pay off the car early without fees.

If you want a professional to handle these high-stakes conversations for you, our financing negotiation service ensures you never pay a penny more than necessary. We act as your seasoned advocate, managing the dealer's offers so you can enjoy a stress-free signing process with total peace of mind.

Professional Advocacy: Why Expert Representation Wins the Financing War

The finance office is often the most intimidating part of the car-buying journey. It's a high-stakes environment where a single signature can cost you thousands in unnecessary interest or hidden fees. Bill Flower provides The Car Coach advantage, bringing 33 years of professional experience from both sides of the desk to protect your interests. This depth of knowledge is essential when weighing dealership financing vs credit union options, as we identify the hidden incentives and markups that a layperson might miss. We act as your seasoned advocate, ensuring your loan terms are optimized for your financial future. We believe you shouldn't have to face this pressure alone.

Our expertise allows us to identify the subtle markups that often go unnoticed by the untrained eye. While you might see a monthly payment that fits your budget, we see the underlying APR and the total cost of credit. Deciding between dealership financing vs credit union options shouldn't be a source of anxiety. We manage the financing negotiation on your behalf, ensuring that the rate you receive is the absolute lowest for which you qualify. By having a seasoned advocate in your corner, you shift the power dynamic back in your favor. This transforms a stressful transaction into a simplified, successful engagement where your needs are the only priority.

A Buffer Between You and the Dealer

Having an expert representative acts as a protective shield against "payment packing" and deceptive markups. We verify every fee and disclosure on the Truth in Lending statement before you ever see the final paperwork. This professional verification gives you the peace of mind that your loan terms are optimized and transparent. We often handle trade-in optimization and financing as a single, cohesive package. This holistic approach prevents the dealer from hiding profit in one area of the deal while appearing to give you a discount in another. You deserve a process where your financial security is the focus, not the dealer's commission. We handle the difficult tasks, allowing you to focus on the excitement of your new vehicle.

Your Next Steps to a Stress-Free Purchase

You can start your car-buying journey with total clarity and confidence. We invite you to a personalized consultation with Bill Flower to discuss your specific needs and goals. Whether you're looking for new or pre-owned vehicle purchase assistance, we provide the expert navigation required to avoid predatory lending tricks. We do the heavy lifting, so you can remain in a position of relaxed enjoyment throughout the entire process. This partnership ensures that every obstacle is removed before you step foot in the dealership. Let The Car Coach handle your next vehicle purchase and financing negotiation.

Drive Forward with Total Confidence

Navigating the choice between dealership financing vs credit union is no longer a source of stress when you have the right strategy in place. You now understand that while dealers offer convenience, they often hide profit in interest markups. By walking into the showroom with a credit union pre-approval, you establish a firm baseline that forces the dealer to compete for your business. We believe you deserve a transparent experience where every dollar is accounted for and every rate is optimized for your benefit.

Bill Flower brings over 33 years of dealership and brokerage experience to your side of the desk. We provide nationwide service for new and pre-owned vehicle procurement, handling the expert negotiation of price, trade-in, and financing so you don't have to. This professional buffer allows you to enjoy the excitement of your new car while we manage the complex details on your behalf. Secure your next vehicle with professional representation; contact Bill Flower today. You've gained the knowledge to protect your financial future. It's time to drive home with a deal that offers true peace of mind.

Frequently Asked Questions

Is it better to get a car loan from a credit union or a dealership?

A credit union is generally the better choice for securing the lowest long-term cost, while a dealership offers superior convenience and access to manufacturer incentives. Credit unions are member-owned cooperatives that prioritize lower APRs and transparency for their participants. Dealerships operate as for-profit retailers that may mark up interest rates to increase their revenue. Choosing between dealership financing vs credit union depends on whether you value a personalized, low-cost loan or a fast, one-stop shopping experience.

Can a dealership really beat a credit union’s interest rate?

Yes, a dealership can beat a credit union's rate specifically when they offer manufacturer-subvented financing. Captive lenders like Ford Credit or Toyota Financial sometimes provide promotional rates, such as 0% or 1.9% APR, to move specific vehicle inventory. These incentivized rates are often lower than what any commercial bank or credit union can provide. However, outside of these special promotions, the dealer's standard rates are typically higher due to built-in profit margins and commissions.

Does getting pre-approved for a car loan hurt my credit score?

Getting pre-approved results in a hard inquiry that may slightly lower your score, but credit scoring models are designed to encourage rate shopping. If you submit all your loan applications within a 14 to 45-day window, they're treated as a single inquiry for scoring purposes. This protective window allows you to compare dealership financing vs credit union offers without damaging your credit health. It's a vital step for establishing a realistic budget before you visit the showroom.

What is a "Buy Rate" in dealership financing?

The Buy Rate is the actual interest rate a lender offers the dealership based on your specific credit profile. This is the raw cost of the money before the dealer adds any additional percentage points for their own profit. Dealers often quote you a higher "Sell Rate" and pocket the difference as a commission. We believe you should always ask to see the Buy Rate to ensure the dealer isn't hiding excessive profit inside your interest rate.

How much can I save by using a credit union for an auto loan?

You can save thousands of dollars over the life of your loan by opting for a credit union's lower interest rates. In May 2026, the average 60-month new car rate is 7.04%, but top credit unions are offering rates as low as 3.89% for members with excellent credit. On a standard $40,000 loan, reducing your APR by 3% can save you over $3,000 in total interest charges. These savings provide significant financial peace of mind.

Should I tell the dealer I have a pre-approval before we agree on a price?

You should wait to reveal your pre-approval until after you have finalized the purchase price of the vehicle. If a dealer knows you aren't using their financing, they might be less flexible on the car's price because they lose their "back-end" profit. By keeping your financing plans private during the initial negotiation, you maintain maximum leverage. This strategy ensures you get the best deal on the car and the loan separately.

What are the most common hidden fees in dealership financing?

The most frequent hidden costs include "Dealer Reserve" rate markups and "payment packing" with expensive add-on products. Dealers may slide items like window etching, fabric protection, or nitrogen-filled tires into your monthly payment without clearly disclosing their individual costs. These products are often marked up by 200% or more compared to their actual value. Always review your Truth in Lending disclosure line-by-line to identify and remove these unnecessary charges before signing.

Is gap insurance cheaper through a credit union or a dealership?

Gap insurance is almost always significantly more affordable when purchased directly through your credit union. Dealerships treat gap insurance as a high-margin retail product and often charge double or triple what a credit union requires for the same coverage. Securing this protection through your financial institution ensures you're covered in the event of a total loss without paying an excessive dealer markup. It's one of the easiest ways to reduce your total loan balance.

To be noted:

This is intended for informational purposes only!